BOSTON, MA – A recent analysis of an 86-year-old’s estate planning efforts has inadvertently unveiled a shocking truth: the average American simply cannot afford the administrative, legal, and financial complexities associated with the dignified cessation of existence. What began as a dutiful effort to secure an aging parent's modest home and savings from the gaping maw of long-term care costs quickly devolved into a systemic exposé of a financial infrastructure primarily serving those with assets in the high eight figures or beyond. The initial foray into simple wills and basic directives quickly escalated into a postgraduate course in asset protection from the very government programs ostensibly designed to help.

"It's like showing up to a Formula 1 race with a unicycle and being told you just need a 'good strategy'," explained Dr. Eleanor Vance, a senior fellow at the Institute for Post-Mortem Economic Inequities, referencing the common American experience. "For most families, 'estate planning' isn't about passing on generational wealth; it's about spending a significant chunk of their remaining time and resources trying to prevent the state from immediately seizing their last $120,000 for a broken hip. The system isn't broken; it's working exactly as designed, just not for you. It's an elaborate gauntlet for the solvent."

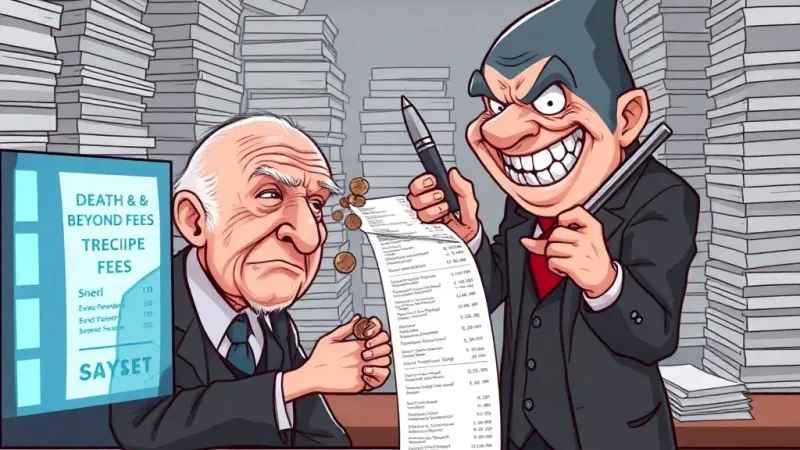

The intricate web of Medicaid asset look-back periods, "spousal impoverishment protections," and "qualified income trusts" has become so labyrinthine that merely understanding it is a full-time job requiring a specific subset of legal expertise. Families are increasingly advised to consult specialists in "Medi-Caid Mitigation and Intergenerational Asset Preservation Negation," a niche field that charges hourly rates comparable to what a senior citizen might pay for a full month of nursing home care. These specialists often operate out of non-descript suburban offices, providing their services with a grim, knowing chuckle. "We often tell clients that if they can afford our fees, they probably don't need us as much as someone who can't," noted Barnaby Finch, a managing partner at the boutique firm of Finch, Finch, and Clawback, LLC. "It's a delightful paradox, isn't it? The cost of protecting your paltry life savings is often more than those savings themselves."

This two-tiered system of financial mortality planning has created a stark divide. While billionaires navigate intricate offshore trusts, dynastic foundations, and philanthropic pseudo-shelters designed to preserve fortunes across centuries and deftly avoid taxation, middle-class families are left to debate whether selling their deceased parent’s 2007 Honda Civic will trigger a six-month disqualification from critical assistance. The unspoken assumption, critics argue, is that if you're not wealthy enough to maintain a private jet and several international residences, you’re simply not sophisticated enough to protect the modest equity in a 3-bedroom suburban ranch home. This forces a desperate scramble, often leading to ethically murky "gifting" strategies or the hasty transfer of assets, all under the looming shadow of government scrutiny.

"The real takeaway from helping my dad isn't about wills or trusts," stated one anonymous family member whose personal account sparked the analysis, wishing to remain unnamed due to ongoing 'pre-bereavement asset restructuring.' "It’s realizing that 'pulling yourself up by your bootstraps' only works if you're rich enough to afford the boots, the straps, and a private legal team to ensure nobody can ever take them from you, even after you're gone. For everyone else, it’s just a scramble to die without bankrupting your children."